Day 5: Sign-Up Bonuses — The Jackpot

NPLB 14-Day Stacking Series

I am not a credit card affiliate. Any credit card link on No Point Left Behind is my own personal referral link for cards I personally use. If you choose to use one, we may both earn a bonus — but I never earn commissions from banks. My advice is always free and based on real strategies my family uses.

One card. One bonus. Enough points for a free round-trip flight.

This is where stacking gets REALLY fun.

Okay, THIS is the day I have been waiting to write.

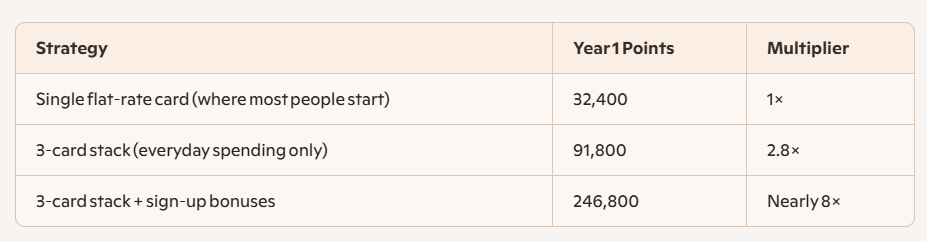

If you've been following along since Day 1, you know we've been building something powerful together. We learned what credit card stacking actually is. We mapped out your spending into categories. We built your first two-card pair and watched the math jump from 32,400 to 79,800 points. We added a catch-all third cardand pushed it to 91,800 points a year. All important. All necessary. All foundational work that sets the stage for what I'm about to show you today.

But today? Today is the FUN part. Today is where a lot of new stackers have their very first "holy cow" moment. And honestly? It never gets old for me either — even after 20+ years of doing this.

So here it is. What if I told you that a single credit card — just one — could earn you enough points for a free round-trip flight... before you even start using it for everyday spending?

That's what a credit card sign-up bonus is. It's a welcome offer from a credit card company that hands you a massive chunk of points just for meeting a minimum spending requirement in the first few months. And when you combine sign-up bonuses with the stacking strategy you've been building all week?

That's when "20–30 free flights a year" stops sounding crazy and starts sounding... completely achievable.

What Is a Credit Card Sign-Up Bonus (And Why Should You Care)?

Let me keep this simple because it really is simple.

When you open a new credit card, most issuers offer what's called a welcome bonus (also called a sign-up bonus). It's a large lump sum of points, miles, or cash back that you earn if you spend a certain amount within the first 3 months — sometimes 6 months. That's it. The card company is essentially paying YOU to try their card.

Let me give you two real examples so the numbers feel concrete:

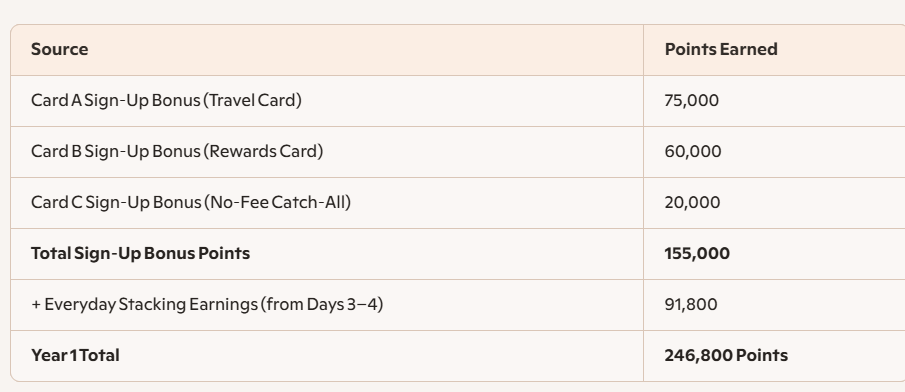

Example A: A popular travel rewards card offers 75,000 bonus points after you spend $5,000 in 3 months. Those 75,000 points? They're worth at least $750 in travel — enough for a round-trip domestic flight for the whole family, or a big chunk of an international ticket. The card has a $95 annual fee, which means you're netting $650+ in travel value from that one bonus alone.

Example B: A no-annual-fee cash back card offers a $250 bonus after just $500 in spending in 3 months. Let that sink in — that's a 50% return on your spend. You'd probably spend $500 on groceries in two weeks anyway!

Here's the part I need you to really hear:

This Is NOT About Spending Extra Money

You're spending money you were ALREADY going to spend — groceries, gas, bills, subscriptions — and getting a massive bonus on top of it just because you used a new card instead of your old one. You're not changing your lifestyle. You're just changing which piece of plastic you swipe.

The Math That Makes Sign-Up Bonuses a Game-Changer

Alright, remember our math from Days 3 and 4? Let's bring it back, because this is about to get really exciting.

We showed that a 3-card stack on normal everyday spending earns about 91,800 points per year. That's already amazing compared to the 32,400 you'd earn with a single flat-rate card. But what happens when each of those three cards also came with a sign-up bonus?

Let's look at a realistic scenario:

Now let's put that in perspective:

Read that bottom row one more time. Nearly EIGHT TIMES the points. From a family that didn't change a single spending habit — they just used different cards.

The family didn't go on a shopping spree. They didn't buy anything they wouldn't have bought anyway. They simply opened three cards instead of one, put their normal spending on the right cards, and the sign-up bonuses did the heavy lifting in Year 1.

THIS is why I say sign-up bonuses are the jackpot. The everyday earning from stacking is your steady paycheck. The sign-up bonuses are your lottery winnings — except you actually get to keep winning, year after year, every time you strategically add a new card to your stack.

How to Meet the Minimum Spend (Without Spending More)

I know what you're thinking right now. I can practically hear it through the screen:

"$3,000 or $5,000 in 3 months? Julie, that sounds like a LOT."

I hear you. When I first saw those numbers, I felt the same way. But then I sat down and actually added up what my family spends in a normal month — groceries, gas, the electric bill, our phone plan, streaming subscriptions, the occasional Target run — and I realized we were already spending well over $2,000 a month without even trying.

Here are practical, realistic strategies to meet minimum spend requirements without spending a single extra dollar:

Put ALL your normal spending on the new card. Groceries, gas, dining out, subscriptions, utilities (if they accept credit cards without a fee). For 3 months, this card is your go-to for everything.

Time your application with a planned big purchase. Need a new appliance? Back-to-school shopping coming up? Holiday gifts? Car insurance premium due? Annual subscriptions renewing? Open the card right before that spending happens naturally.

Pay bills you already have. Phone bill, internet, streaming services, insurance premiums — many of these can be put on a credit card. You're paying them anyway. Might as well earn a bonus while you do it.

Prepay expenses you know are coming. Stock up on gift cards at the grocery store for places you already shop — Amazon, Target, your favorite restaurant. You're going to spend that money eventually.

Offer to pay for a group dinner. Pick up the tab, have your friends Venmo you back. You get the spend toward your bonus. They get the convenience of not splitting a check. Everybody wins.

The Golden Rule of Minimum Spend

NEVER spend money you wouldn't have spent anyway just to hit a bonus. If you're buying things you don't need, you're not earning free travel — you're paying for it. The points aren't worth it if you're going into debt or blowing your budget. The whole point of this strategy is that it fits INTO your life, not that you rearrange your life around it.

Timing Your Applications — The Stacking Calendar

Here's where we get a little more strategic. Sign-up bonuses are amazing, but when you apply matters almost as much as which card you pick. Think of it as a calendar, not a sprint.

Space your applications 3–6 months apart. Each application triggers a hard credit inquiry on your report. One or two inquiries are no big deal — your credit score might dip by a few points temporarily and bounce right back. But five applications in one month? That's going to raise some eyebrows. Give yourself breathing room.

Don't apply for 2 cards from the same issuer too close together. Some issuers have specific rules about how many cards you can open in a certain timeframe. Chase, for example, has what's known as the "5/24 rule" — they'll generally decline you if you've opened 5 or more new cards (from any issuer) in the past 24 months.

Time applications before your big spending periods. This is my favorite trick. I know that August means back-to-school spending. November and December mean holiday shopping. Summer means vacation expenses. So I time my new card applications right before those natural spending peaks. The minimum spend practically takes care of itself.

♥ What I Actually Do: The Tuition Hack

Here’s one of my favorite moves: I time my sign-up bonuses around when tuition is due for my boys. Tanner and Finn both have scholarships that cover most of their college expenses — but there’s still a balance we pay out of pocket. Our college doesn’t charge a fee for credit card payments (this is HUGE — always check yours!), so when tuition is due, I put the remaining balance on whatever new card I’m working on hitting a sign-up bonus for.

Then we file for reimbursement from their 529 plans. So the money comes back to us, the minimum spend gets met, and those bonus points land in my account. It’s a big chunk of spending I was going to do anyway — I just made sure a sign-up bonus was waiting for it.

If you have college tuition, insurance premiums, property taxes, or any other big predictable bill coming up — THAT is when you open a new card.

Watch for elevated bonus offers. Card issuers periodically increase their welcome offers. A card that normally offers 60,000 points might bump it to 80,000 for a limited time. If you can wait for a higher offer, it's worth it. But here's my caveat: don't wait forever. A good bonus today beats a maybe-better bonus someday. I've seen people wait so long for a "perfect" offer that they missed out on a year's worth of points.

Think about it as a yearly cycle. I personally apply for about 2–3 new cards per year, timed strategically around our family's natural spending rhythms. That's enough to keep the sign-up bonuses flowing without going overboard.

★ What I Do — Julie's Sign-Up Bonus Strategy

Okay, I have to be honest — this is the part of travel hacking that makes me light up. If you could see my face right now while I'm writing this, I'm grinning. This is MY thing.

Here's how I think about it: every year, I look at which cards have the best welcome bonuses, and I time my applications around our family's natural spending cycles. Back-to-school? That's a great time to open a new card — we're buying supplies, clothes, and paying fees anyway. Holidays? Another natural high-spend window. I don't force spending. I just redirect spending I was already doing toward a new card for the first few months.

Remember my parents' Marriott card from yesterday? That's a sign-up bonus play. They picked it up specifically for the welcome offer — a huge chunk of Marriott points that we used toward hotel stays. They didn't change how they spend. They just put their normal purchases on the Marriott card for a few months, hit the bonus, and moved right back to their regular 3-card rotation. Simple.

And here's the thing that I think surprises people most: when I say my family earns 20–30 free round-trip tickets a year, sign-up bonuses are a HUGE part of how we do it. The everyday stacking earns us a steady flow of points, but the sign-up bonuses are what push us into "we literally cannot spend points fast enough" territory. I'm not exaggerating — some years we've had so many points that we've genuinely struggled to use them all before they'd expire or devalue.

I've paid for exactly ONE plane ticket with cash since 2019. One. My son Tanner hopped on a trip last minute, and even though I had the points, it was actually cheaper to just pay cash that one time. Every other flight since 2019? Free. That's me, Brandon, Tanner, Finn — plus trips with my parents and my best friends. Sign-up bonuses are the engine that makes that possible.

There is no wrong or right way to do this. The cards that work for me might not be the best for you. However, these are the strategies I have used year after year — and they work.

What to Watch Out For

I always want to be straight with you, so here are a few things to keep on your radar:

1. Annual fees. Some cards with the best sign-up bonuses come with annual fees. That's not automatically a deal-breaker — a $95 fee on a 75,000-point bonus is a no-brainer when those points are worth $750+ in travel. But you should always factor the fee into your decision. And guess what? We're covering exactly how to evaluate annual fees in Day 6 — tomorrow. Perfect timing.

2. Minimum spend traps. Don't overextend yourself. If the minimum spend is $5,000 in 3 months and you normally only spend $2,000 a month, that card might not be right for you right now. There's no shame in choosing a card with a lower threshold. A $200 bonus you can easily earn beats a $750 bonus that stresses you out.

3. The "churn" temptation. Some people open cards constantly — grab the bonus, close the card, open a new one, repeat. This can work, but it's an aggressive strategy and it can impact your credit if done carelessly. I don't recommend it for beginners. Build your stack thoughtfully. Add cards that actually earn their place in your wallet for the long term.

4. Read the fine print. Some issuers won't give you a bonus if you've had the same card before (or a card in the same product family) within a certain period — sometimes 24 months, sometimes 48 months. Always check the terms before you apply. It takes 30 seconds and can save you from a wasted application.

Quick Tip

Before you apply for any card, search online for "[card name] sign-up bonus eligibility rules." You'll quickly find out whether there are any restrictions that apply to you. Two minutes of research can save you a wasted hard inquiry on your credit report.

✎ Today's Homework

Here's your assignment — and it's a fun one today:

Go look at the cards you identified in Days 3 and 4 — your two bonus category cards and your catch-all. Now look at their current sign-up bonuses. What are they offering right now?

Write down three things for each card:

The bonus amount (points, miles, or cash back)

The minimum spend requirement

The time limit to meet it (usually 3 or 6 months)

Then do some quick math: based on your spending map from Day 2, could you meet that minimum spend naturally — without buying a single thing you wouldn't have bought anyway?

If the answer is yes, that's a strong candidate for your stack.

DON'T APPLY YET. Tomorrow in Day 6we're covering annual fees, and you'll want that information before you commit to anything. But now you know the numbers — and knowledge is power.

Remember — there's no wrong way to do this. A $200 bonus that fits your budget is worth MORE than a $750 bonus that makes you overspend. The best bonus is the one you can earn without changing how you live.

Cards Worth Looking At

I get asked all the time: "Julie, which cards should I start with for my first sign-up bonus?"

Here are a few types of cards that I've personally used and that tend to have strong welcome offers. I'm not listing specific bonus amounts here because those change all the time — but I'll tell you what to look for.

Full disclosure: some of the links below are personal referral links, which means I may earn a small commission or bonus if you apply — at no extra cost to you. I only recommend cards I've personally used and believe in. You'll never see me push a card just because it pays me well. That's not how I operate.

A solid travel rewards card with a big welcome bonus. Look for cards offering 50,000–75,000+ points after a reasonable minimum spend. These are your heavy hitters — one bonus can be worth an entire round-trip flight. Some come with annual fees in the $95 range, which we'll evaluate tomorrow.

If you’re looking for a strong travel rewards card with a big welcome bonus, here’s the one my family has used for years: 👉 My Travel Rewards Card Referral Link

This is the type of card that helped us earn our first free flights. The welcome bonus alone can often cover a round‑trip ticket, depending on where you’re going.

A flexible cash back or points card with no annual fee. These usually offer smaller bonuses ($150–$250) but with very low minimum spend requirements — sometimes just $500. These are fantastic starter cards and perfect catch-all cards for your stack. My sons Tanner and Finn both have cards like this.

If you want a simple, no‑annual‑fee starter card (the kind my boys Tanner and Finn use), here’s the one we personally like: 👉My No‑Annual‑Fee Starter Card Referral Link

These cards are perfect as your “catch‑all” in a stacking setup — low minimum spend, easy bonus, and great for everyday purchases

A hotel or airline co-branded card for a specific goal. If you have a trip in mind — say, you want free hotel nights at a specific chain — a co-branded card's sign-up bonus can get you there fast. My parents' Marriott card is a perfect example — their sign-up bonus came with 5 free night certificates. Not points on a screen — actual free hotel nights. I picked up the same card and used my free night certificates to book my family a trip to Yosemite. That's the kind of sign-up bonus that makes you want to hug your mailbox when the card arrives.

A Note About Recommendations

I will never tell you that one specific card is "the best" — because the best card depends entirely on YOUR spending, YOUR goals, and YOUR family. What works beautifully for my family might not be the right fit for yours. I share what I use so you have a starting point, but you get to build the stack that fits your life.

What's Coming Next

Tomorrow we tackle one of the most common questions I get: "Is the annual fee worth it?"

Day 6 is all about evaluating annual fees — when to pay them, when to walk away, and how I personally decide every single year which cards to keep and which to let go.

Spoiler: I re-evaluate EVERY card, EVERY year. No card gets a free pass. Not even my favorites. I'll show you exactly how I make that call — and it's way simpler than you'd think.

See you tomorrow!

About the Author

Julie Davis has been travel hacking for over 20 years — long before anyone she knew was doing it. She's paid for exactly ONE plane ticket with cash since 2019 — her son Tanner hopped on a trip last minute and even though she had the points, it was cheaper to pay cash that one time. Every other flight? Free. Her family regularly earns 20–30 free round-trip tickets a year on points alone, plus countless hotel rooms. In 2024, she added casino cruises to her travel hacking playbook.

Julie loves traveling with her husband Brandon, her sons Tanner and Finn, her parents, and her best friends — because the best part of free travel is who you get to share it with.

She created No Point Left Behind to prove that travel hacking isn't complicated — it's just a skill nobody taught you yet.

Want to learn alongside thousands of other moms? Join Julie's free Facebook community, Travel Hacking Moms Group, where she shares real-time tips, wins, and answers your questions every day.