Day 3 - Your First Stacking Pair: The Starter Kit

Day 3 of the NPLB 14-Day Stacking Series — Two cards. That's all you need to start earning serious rewards on the spending you're already doing.

If you did your homework yesterday, you should be sitting there with a piece of paper (or a note on your phone) with your top three spending categories and an approximate monthly dollar amount for each. That little list is more powerful than you think.

Because today? Today is the day we stop just looking at our spending and start putting it to work. Today we're building your very first credit card stacking pair — and I promise you, it's easier than you think.

You don't need five cards. You don't need to be a finance expert. You don't need to change a single thing about how you spend. You need two cards that complement each other. And remember — there's no perfect pair. There's only YOUR pair. The one that matches YOUR spending and YOUR life. There is no wrong or right way to do this. The cards that work for me might not be the best for you. But the strategies I'm about to share? I've used them year after year, and they've earned my family more free flights than I can count.

Heads up — some links in this post are personal referral links. If you apply and are approved for a card through my link, I may earn bonus points from the card issuer — at no extra cost to you. I only share cards I personally carry and use. Thank you for supporting No Point Left Behind!

What Is a Stacking Pair?

A credit card stacking pair is simply two credit cards that work together to cover your biggest spending categories at bonus rates — instead of earning a flat 1x on everything with a single card.

Think of it like shoes. You wouldn't wear heels to the gym or sneakers to a wedding, right? You match the shoe to the occasion. Stacking pairs work the exact same way — you match the card to the purchase.

Here's the core principle:

Card A covers your #1 spending category at a bonus rate (3x–6x points per dollar)

Card B covers your #2 spending category at a bonus rate (3x–5x points per dollar)

Together, those two cards turn the spending you're already doing into significantly more points. No extra spending required. No complicated system. Just a different card at checkout.

That's it. That's the whole concept. Two cards. Two categories. Way more points.

How to Build YOUR First Pair (Step by Step)

Grab your spending map from Day 2 and let's walk through this together. I want you to treat this like we're sitting at my kitchen table working through it over coffee.

Step 1: Look at Your Top Two Spending Categories

Pull up the homework you did yesterday. What were your top two spending categories? For most families, they're usually some combination of groceries, dining, and gas. That's totally normal — that's where family life happens. Soccer practice drive-throughs, weekly grocery runs, the gas station on repeat.

Whatever yours are, write them down side by side. We're about to find a card for each one.

Step 2: Find a Card That Earns 3x or More on Your #1 Category

This is your workhorse card — the one you'll reach for the most. You want a card that earns bonus points in your biggest spending category.

If groceries is your #1: Look for a card that earns 3x–6x at supermarkets. These are everywhere, and some of the best rewards cards on the market target this exact category.

If dining is your #1: Look for a card that earns 3x–4x at restaurants. Dining is one of the most common bonus categories — lots of great options here.

If gas is your #1: Look for a card that earns 3x–5x at gas stations. Several cards offer strong gas rewards, especially for families with long commutes.

If online shopping is your #1: Look for a card that earns bonus points on online retail purchases. Some cards offer rotating 5x categories that include online shopping.

You don't need to apply today. Just start looking at what's out there. (We'll talk about timing your applications in Day 5 — that's a big one.)

Step 3: Find a Second Card That Covers Your #2 Category

Now find a card that earns bonus rewards on your second biggest spending category — and here's the key: it should cover a DIFFERENT category than Card A.

That's the whole point of stacking. If Card A handles groceries, Card B should handle dining (or gas, or online shopping). Together, they cover more ground than either one could alone.

Step 4: Make Sure You Have a Safety Net

Here's a step people forget: make sure at least one of your two cards earns a decent flat rate — 1.5x to 2x — on everything else. That way, when you make a purchase that doesn't fall into either bonus category (think: Target, the vet, your kid's school fundraiser), you're still earning more than the standard 1x.

This flat-rate "safety net" is what keeps you covered until you add a third card in Day 4. For now, it makes sure no purchase gets left behind at just 1 point per dollar.

The Math That Changes Everything

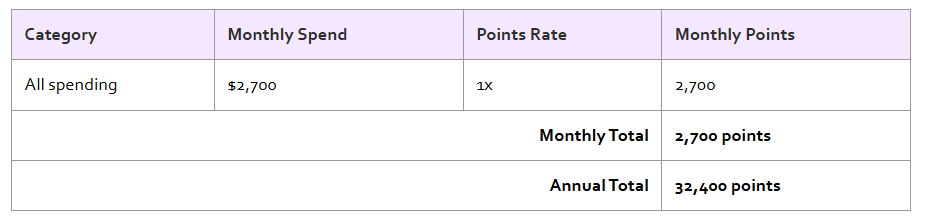

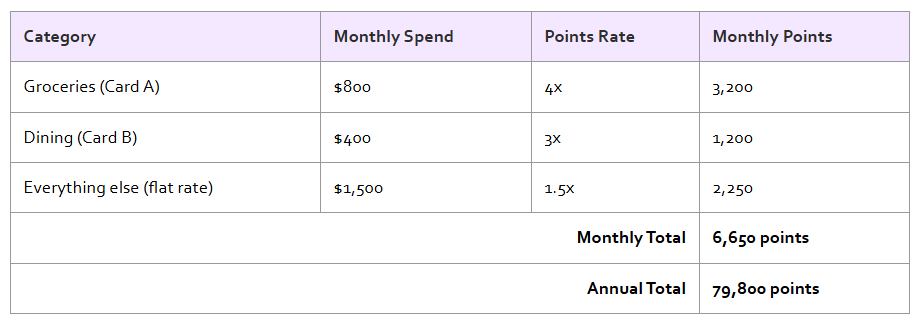

Okay, let's make this real. Remember the sample family budget from Day 2? Let's see what happens when we go from one card to two.

BEFORE: One Card, 1x on Everything

AFTER: Two-Card Stacking Pair

Read that again. Almost 2.5 times the rewards. That's enough for a round-trip domestic flight or two — from spending you were ALREADY doing. The only thing that changed was which card you pulled out of your wallet at checkout.

That's the magic of stacking.

"When I first figured out that just using two different cards could nearly triple my points, I was equal parts thrilled and frustrated. Thrilled because — free flights. Frustrated because I'd been leaving those points on the table for YEARS. I'd been putting everything on one card like a robot, earning 1x on every single purchase, and basically throwing away thousands of points a year. But here's the thing I tell myself and I'll tell you: the best time to start stacking was years ago. The second best time is today."

💜 What I Do — My First Stacking Pair

I honestly don't remember ever calling it "stacking" back then. I'd been travel hacking for over 20 years — years ago, before there was much info out there about any of this — and for the longest time I'd get a new card and put everything on it. Every single purchase. One card for everything.

Then one day I noticed that one of my cards earned bonus points at grocery stores and another earned bonus points on dining. And I thought, wait — what if I just used the right card at the right place? That was my aha moment. I started using one card for groceries and a different card for restaurants, and my points jumped almost immediately. It wasn't fancy. It wasn't complicated. It was just — intentional.

That simple two-card setup is what started me down this path. Today, my system is more advanced — as I mentioned in Day 2, I actually split my grocery spending between two different cards depending on the rewards structure. But it ALL started with matching two cards to two categories. That's where the stacking magic begins.

And here's something worth mentioning: my boys Tanner and Finn each have a Chase Freedom Unlimited — and even though it's technically one card, it covers dining at 3% and everything else at 1.5%. If you're truly just starting out and only want one card before you build a pair, a card with that kind of structure is a solid foundation. But when you're ready for two? That's when the rewards really start to multiply.

Common Mistakes to Avoid

Before you start browsing cards, let me save you from a few stumbles I've seen (and, honestly, made myself over the years). None of these are deal-breakers — but avoiding them will make your stacking journey smoother from the start.

Don't overthink it. Your first stacking pair doesn't have to be perfect. It really doesn't. You can swap cards later. You can adjust as your spending changes. The important thing is to START. A good pair today beats a "perfect" pair you never get around to building.

Don't apply for both cards on the same day. Space your applications out by at least a few months. Each application triggers a hard credit inquiry, and spacing them out is better for your credit score. (We're going to get into application timing in Day 5 when we talk about sign-up bonuses — it's a whole strategy unto itself.)

👉Most beginners apply for one card every 1–3 months — that’s normal and healthy.

Don't pick two cards with the same bonus category. If both cards earn bonus on dining, you've doubled up on one category and left everything else at 1x. The whole point of a stacking pair is coverage across DIFFERENT categories. Think peanut butter and jelly — not peanut butter and peanut butter.

Don't forget to check the annual fee. Some amazing rewards cards have annual fees — and that's okay. Sometimes they're absolutely worth it. We'll cover exactly when annual fees make sense and when they don't in Day 6. For now, just make sure you know what you're signing up for before you apply.

Don't change your spending to "match" your cards. This is a big one. Stack your cards around your EXISTING spending. Never spend more just because a card earns bonus in a category. The points aren't worth it if you're overspending to earn them. The whole beauty of stacking is that you earn more from spending you were going to do anyway.

📝 Your Day 3 Homework

Here's your assignment: Using your spending map from yesterday, identify the TWO categories where you spend the most. Then start looking for cards that earn 3x or more in those categories.

You don't have to apply today — just start looking. Browse, compare, make a shortlist. Get curious. Look at what bonus categories different cards offer and start imagining how two of them could work together for YOUR spending.

Tomorrow in Day 4, we're adding a third card to fill the gaps. And in Day 5, we'll talk about how to time your applications to maximize sign-up bonuses (this is where it gets really exciting). The pieces are coming together.

And remember — your pair is YOUR pair. It doesn't have to look like mine or anyone else's. The best stacking pair is the one that matches your life.

What's Coming Next

Tomorrow we take your two-card pair and add a third card — the catch-all that sweeps up everything your first two cards don't cover. This is the 3-card sweet spot, and it's where stacking goes from "smart" to "wait — how are you flying for free?"

Trust me, you're going to want to see this one.

Wondering which specific cards I use and recommend? I'll be sharing my full card lineup with links as we get deeper into the series. For now, focus on finding YOUR best pair — the right cards for YOUR spending. That's the foundation everything else is built on.

Series Navigation:

Previous: Day 2: Know Your Spending Categories

🎯 You're Reading the NPLB 14- Day Build Your Credit Card Line Up Series

Every day for 14 days, Julie is breaking down her build your credit card line Up Series — from absolute beginner to booking free trips. Don't miss a single day.

Follow along: Join Travel Hacking Moms Group on Facebook for daily posts, live Q&A, and a community of moms who are stacking their way to free travel.

Start from the beginning: Build Your Credit Card Line Up Series

About the Author

Julie Davis has been travel hacking for over 20 years — long before anyone she knew was doing it. She's paid for exactly ONE plane ticket with cash since 2019 — her son Tanner hopped on a trip last minute and even though she had the points, it was cheaper to pay cash that one time. Every other flight? Free. Her family regularly earns 20–30 free round-trip tickets a year on points alone, plus countless hotel rooms. In 2024, she added casino cruises to her travel hacking playbook.

Julie loves traveling with her husband Brandon, her sons Tanner and Finn, her parents, and her best friends — because the best part of free travel is who you get to share it with.

She created No Point Left Behind to prove that travel hacking isn't complicated — it's just a skill nobody taught you yet.

Want to learn alongside thousands of other moms? Join Julie's free Facebook community, Travel Hacking Moms Group, where she shares real-time tips, wins, and answers your questions every day.