Adding a Third Card: The Power Play

NPLB 14-Day Stacking Series • Day 4 of 14

The third card is where the magic happens. It catches everything your first two miss — and makes sure no dollar earns less than 2x.

By Julie Davis • NoPointLeftBehind.net • April 21, 2026 • 10 min read

Yesterday, you built your first stacking pair, and if the math blew your mind — going from 32,400 points a year to nearly 80,000 just by using two cards strategically — buckle up. Because today we're about to take it even further.

Two cards are great. Seriously great. But here's the thing: your two-card pair is covering your top two spending categories at beautiful bonus rates. What about everything else? Think about all those purchases that don't fit neatly into "groceries" or "dining" — clothing for the kids, Target runs, Amazon orders, your electric bill, that Home Depot trip, the vet bill, back-to-school supplies, medical co-pays. Right now, all of that spending is earning you 1x or maybe 1.5x. That's points just sitting there, waiting to be picked up.

That's where the third card comes in. The catch-all. The safety net. The card that makes sure NOTHING you buy earns less than 2x. This is the move that separates casual rewards earners from families who are flying for free — and I mean actually, genuinely, boarding-the-plane-with-zero-dollars-spent free

Ideally, your catch‑all earns 2x, but 1.5x is still a huge upgrade over 1x — especially if it earns a points currency you value more, like I personally do with Ultimate Rewards. The “best” card is the one that fits your ecosystem, not the one with the biggest number.

This post contains affiliate links. If you use them, I may earn a small commission at no extra cost to you. I only share cards, tools, and strategies my family actually uses to earn free travel. Your support helps keep No Point Left Behind free and full of practical guides for everyday travelers.

Why Three Cards Is the Sweet Spot

Here's the beautiful simplicity of a three-card stack:

Card 1 covers your #1 spending category at 3x–6x (probably groceries)

Card 2 covers your #2 spending category at 3x–5x (probably dining or gas)

Card 3 covers everything else at a flat 2x

That means every single dollar you spend is working at 2x or better. No money left earning 1x. No points left on the table. No point left behind — see what I did there?

And here's what I love most about the three-card setup: it's manageable. You're not juggling a wallet full of plastic. You're not standing at the register trying to remember which card gets you 4x at office supply stores on the third Tuesday of months that start with "J." You have three cards, and each one has a clear job. That's it.

Most people can remember three cards easily: "This one for groceries, this one for dining, this one for everything else." Simple enough that you don't even have to think about it after the first week or two.

A note on growing beyond three:

Some people eventually add 4, 5, or even more cards to their stack as they get comfortable — I'll be honest, I have more than three myself these days. But three is where you should live until the system feels effortless. Master three before you add more. There's no prize for having the most cards in your wallet. The prize is the free flights. And three cards gets you there.

♥ Real-World Proof: My Parents’ 3-Card Stack

My mom and me summer of 2025 - Alaska cruise we used points and miles for their flights and pre-hotel stay

Want proof that three cards is enough? Look at my parents. They’re retired, they travel often, and they have zero interest in managing a complicated system. Their stack is simple: a Chase Sapphire Preferred, a Capital One Venture Card, and right now a Marriott card they picked up for a sign-up bonus. That’s it. Three cards. And we get nearly all their flights and hotel rooms covered on points and miles. They don’t want any more credit cards — and they don’t NEED any more. The system works beautifully for them. So when I say three cards is the sweet spot, I mean it. For some people, three cards isn’t just the starting point — it’s the whole game plan. And that’s perfectly fine.

What Makes a Great Catch-All Card

Not just any card works as your third card. Your catch-all needs to be a workhorse — the card you pull out for everything that isn't covered by your first two. Here's what to look for:

Earns a flat 2x (or at minimum 1.5x) on ALL purchases — no category restrictions, no quarterly activation, no spending caps. Every purchase, every time, same rate.

No annual fee (or a very low one) — since this card is covering your miscellaneous spending, you don't want to be paying a big annual fee for the privilege. This should be a card that earns its keep just by being in your wallet.

Ideally earns rewards in the same currency as one of your other cards — this is a bigger deal than it sounds. Let me explain.

When I say "same currency," I mean that if two of your cards earn points in the same rewards program — say they both earn Chase Ultimate Rewards, or they both earn Citi ThankYou Points — you can pool those points together into one big bucket. And a bigger bucket of points means more flexibility when it comes time to book travel. Instead of having 30,000 points scattered across three different programs, you've got 60,000 or 80,000 points in one place, which is often enough for a round-trip flight or a really nice hotel stay.

We'll dig deeper into this on Day 8 when we talk about transferable points ecosystems. For now, just keep it in the back of your mind as a nice-to-have.

There are several great catch-all cards out there — some offer a flat 2% cash back on everything, others offer 1.5x to 2x in transferable points on every purchase. The right one for you depends on which rewards ecosystem you're building in. There is no wrong or right answer here. The cards that work for me might not be the best for you. But the strategy is the same: cover what your first two cards don't.

The Complete 3-Card Stack in Action

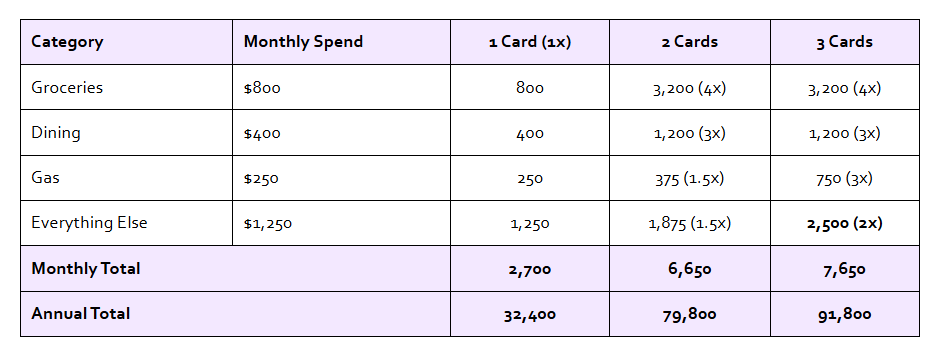

Okay, this is the part I've been excited about all day. Let's go back to our sample family budget from Day 2 and see what happens when we add that third card to the stack.

Remember this family? They spend about $2,700 a month across a pretty typical mix of categories. Here's how their points earning has evolved over the past three days:

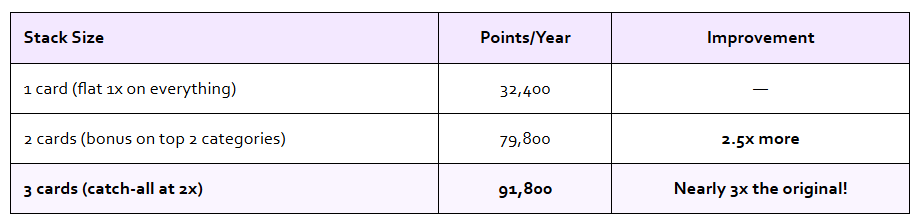

The Progression: 1 Card → 2 Cards → 3 Cards

Let that sink in for a second.

That extra 12,000 points a year from adding just one more card could be a free hotel night or put you over the threshold for another flight. And you STILL haven't changed a single thing about how you spend. Same groceries. Same dinners out. Same gas. Same Amazon orders. You're just using a different piece of plastic at checkout — and earning nearly three times the rewards.

This is the part where people usually say, "Wait… it's really that simple?" Yes. It really is.

What I Do: My Catch-All

✈ Julie's Take

I'll be honest — my setup today is more than three cards because I've been doing this for over 20 years and I've built up my stack over time. But when I think back to my "three-card sweet spot" phase, that's when things really clicked for me.

I had one card for groceries, one for dining and travel, and one flat-rate card that caught everything else at 2x. It was simple, it was manageable, and it was earning us WAY more than the single-card approach I'd been using for years before that. Looking back, the jump from two cards to three was the moment I went from "okay, this is kinda cool" to "oh my gosh, we're actually going to fly somewhere for free."

If you're just building your first stack, three cards is the perfect place to live for a while. You can always add more later — and trust me, you will — but there's no rush. Three gets you 90% of the way there.

And here's a little secret — remember those Chase Freedom Unlimited cards I got for Tanner and Finn back on Day 2? At 1.5% on everything else, those are already acting as their catch-all card. For a college kid who mostly eats out and buys random stuff, a card with 3% on dining and 1.5% on everything else IS a two-card stack built into one. Not bad for their first card, right?

Eventually, they might add a second card for groceries — but honestly, for where they are right now, that single card is doing a lot of heavy lifting. And all those points transfer right back to me. (I told you — no point left behind. I mean it.)

How to Decide Which Card Goes Where

So you've got three cards (or you're planning to). Now the practical question: how do you remember which card to use where? Let me give you the simplest system in the world.

The Wallet Rule

Think of your three cards as employees. Each one has an assigned job. No confusion, no overlap, no guessing at the register.

Card A = Your #1 spending category (probably groceries) → Always use this at the grocery store. That's its only job.

Card B = Your #2 spending category (probably dining or travel) → Always use this at restaurants and for travel bookings. That's its only job.

Card C = Everything else → This is your DEFAULT card. If you're not at a grocery store or a restaurant, pull this one out. Every time. No thinking required.

That last part is key: Card C is your default. It's the card you reach for without thinking. The other two only come out in their specific spots. This makes the whole system almost automatic.

💡 Quick Tip

Some people label their cards with a tiny sticker or set their phone wallpaper to a simple reminder of which card to use where. It sounds silly, but it works — especially in the first couple of weeks before it becomes automatic. I used this trick myself early on! Once I moved beyond three cards, I started using an app called CardPointers to keep track of which card to use at every store. But for three cards? A simple mental system — or a sticky note in your wallet — works perfectly fine.

Common Questions

"Won't having three cards hurt my credit score?"

This is the question I get the most, and I love answering it because the truth is actually the opposite of what most people expect. Having multiple cards can help your credit score — as long as you're paying them off in full every month (and you should always, always be doing that).

Here's why: more cards means more available credit, which means a lower credit utilization ratio. And credit utilization is one of the biggest factors in your credit score. If you have $10,000 in available credit and you're using $2,000, that's 20% utilization. Add another card with a $5,000 limit, and that same $2,000 in spending drops to about 13% utilization — which looks better to the credit bureaus. We'll talk more about credit score myths on Day 7, so hang tight.

"What if I can't get approved for a third card right now?"

That's totally fine! Start with two. A two-card stack is still earning you significantly more than one card — we proved that yesterday. When you're ready, and when your credit profile supports it, add the third. There is no timeline here. No rush. No pressure.

Remember my core philosophy: there is no wrong or right way to do this. The cards that work for me might not be the best for you. The pace that works for me might not be the best for you. Build your stack at your speed.

"Should all three cards be from the same bank?"

Not necessarily — but there ARE advantages to staying within the same rewards ecosystem. Remember what I said earlier about pooling points? If two or three of your cards earn points in the same program, you can combine them into one big bucket. That's powerful.

But it's not a requirement. Plenty of people run a great three-card stack with cards from two or three different banks. We'll dig into the strategy of rewards ecosystems on Day 8when we talk about transferable points. For now, just focus on getting the best bonus rates for your top spending categories. That's the priority.

Your Day 4 Homework

📝 Today's Assignment

Look at your two-card pair from yesterday and identify the gap. What spending ISN'T covered at a bonus rate? That's where your catch-all card goes.

Start browsing flat-rate cards that earn 2x on everything — no annual fee, no category restrictions, just a solid flat rate on every purchase. Look at what's out there. Read some reviews. Compare a few options.

But do NOT apply yet.

InDay 5, we're going to talk about sign-up bonuses — and trust me, you're going to want to read that BEFORE you apply for anything. The timing matters. A lot.

Your three-card stack doesn't have to be perfect. It just has to be YOURS.

What's Coming Tomorrow

Tomorrow is one of my favorite days in the whole series — Day 5: Sign-Up Bonuses (The Jackpot).

This is where stacking gets REALLY exciting, because those welcome offers on new cards? They can be worth hundreds of dollars in free travel by themselves — sometimes even more. I'll show you how to time your applications for maximum bonus value, and why applying for the right card at the right time can be the difference between 50,000 bonus points and zero.

You're not going to want to miss this one.

💳 Want to know my exact cards?

Want to know which specific cards I use in my own stack? I'll be sharing my full lineup with links soon — Day 8is going to be a good one. For now, focus on building YOUR three-card foundation. The strategy matters more than the specific cards.

Navigate the Series:

← Day 3: Your First Stacking Pair (The Starter Kit)

→ Day 5: Sign-Up Bonuses (The Jackpot) —

Every day for 14 days, Julie is breaking down her complete credit card stacking strategy — from absolute beginner to booking free trips. Don't miss a single day.

Follow along: Join Travel Hacking Moms Group on Facebook for daily posts, live Q&A, and a community of moms who are stacking their way to free travel.

About the Author

Julie Davis has been travel hacking for over 20 years — long before anyone she knew was doing it. She hasn't paid for a single plane ticket with cash since 2019, and her family regularly earns 20–30 free round-trip tickets a year on points alone, plus countless hotel rooms. In 2024, she added casino cruises to her travel hacking playbook.

Julie loves traveling with her husband Brandon, her sons Tanner and Finn, her parents, and her best friends — because the best part of free travel is who you get to share it with.

She created No Point Left Behind to prove that travel hacking isn't complicated — it's just a skill nobody taught you yet.

Want to learn alongside thousands of other moms? Join Julie's free Facebook community, Travel Hacking Moms Group, where she shares real-time tips, wins, and answers your questions every day.