Is Travel Hacking Safe? What No One Tells Beginners

The honest truth about credit scores, real risks, and why this strategy changed my family's life.

Travel hacking starts with a plan — not a leap of faith.

📋 In This Post

• What Is Travel Hacking, Really?

• The #1 Fear: Will This Destroy My Credit Score?

• What No One Tells You: The Honest Risks

• The Lazy Girl Approach: Travel Hacking Without Opening New Cards

• 20 Years of Proof: Why I Trust This Strategy

• How to Start Safely: A Beginner Checklist

• FAQ: Your Biggest Travel Hacking Safety Questions

• The Bottom Line

Every time I tell someone I travel hack, I can see it on their face — the pause, the slight head tilt, then: "But isn't that... risky?"

I get it. I really do. The phrase "travel hacking" sounds like something that should come with a hoodie, a dark basement, and a really fast internet connection. It sounds like you're getting away with something. And when something sounds too good to be true, most smart people pump the brakes.

That instinct? It's a good one. You should absolutely ask questions before diving into anything that involves your credit score and your money.

But here's what I want you to know: after 20+ years of travel hacking and 12–15 trips per year, my credit score is excellent. Our finances are solid. And travel hacking has been, hands down, one of the best financial decisions our family has ever made.

So today, I'm going to give you the honest, unfiltered truth — the good, the real risks, and the stuff that nobody else seems to want to talk about. No gatekeeping. No jargon. Just a straight conversation from someone who's been doing this long enough to know what actually matters.

Let's get into it.

Disclosure: This post contains an affiliate link to CardPointers, a tool I personally use and love. If you sign up through my link, I may earn a small commission at no extra cost to you. There are no credit card affiliate links in this post. I'm not a financial advisor — just a travel-hacking mom sharing what's worked for our family over 20+ years. Everything here is for educational purposes and shouldn't be taken as personal financial advice. Full disclosure policy

✈️ What Is Travel Hacking, Really?

Let's clear something up right away: travel hacking is not illegal. It's not a loophole. It's not some shady underground trick that's going to land you on a government watchlist.

Travel hacking is simply being strategic about how you earn and use credit card points, airline miles, and hotel loyalty rewards to travel for less — or even free.

That's it. That's the whole thing.

Banks and credit card companies want you to sign up for their cards. They literally spend billions of dollars on marketing to get you through the door. When you earn a welcome bonus or use a shopping portal, you're not gaming the system — you're playing the game they designed, just smarter than the average player.

Here's what travel hacking actually includes:

Earning welcome bonuses by meeting minimum spend requirements on new cards

Using shopping portals (like Rakuten or airline-specific portals) to earn extra points on purchases you're already making

Stacking deals — combining a portal bonus + a credit card category bonus + a sale price

Choosing the right card for the right purchase (groceries on your 6x card, dining on your 3x card)

Redeeming strategically — knowing when points are worth 1 cent vs. 4+ cents each

Joining free loyalty programs for airlines and hotels to earn points on every stay and flight

💡 Here's the part most people miss:

Most of what I teach at No Point Left Behind doesn't even require opening new credit cards. Shopping portals, dining programs, loyalty accounts, deal stacking — these are all things you can start doing today with what you already have.

How to earn points without opening new cards → How to Earn Points Without Opening a New Credit Card (Beginner Guide)

💳 The #1 Fear: Will This Destroy My Credit Score?

This is the big one. The question I hear more than any other. And I'm going to give it the thorough answer it deserves, because your credit score matters and you deserve real information — not hand-waving.

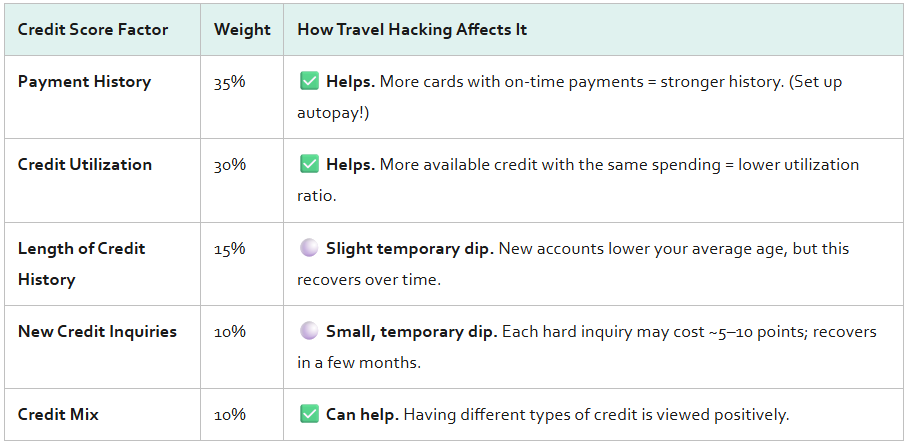

Your credit score is calculated based on five factors. Understanding these is the key to understanding why travel hacking, done responsibly, actually helps most people's credit:

Let's look at the math. Opening a new card causes a small, temporary dip — usually 5–10 points from the hard inquiry. That recovers in a few months. But here's what happens on the other side: travel hacking improves two of the biggest factors — payment history and credit utilization — which together make up 65% of your score.

Here's a quick example to show you what I mean:

The net result? Most responsible travel hackers see their credit scores improve over time. Experian has noted that using credit cards strategically with responsible habits — paying on time, keeping balances low — isn't bad for your credit in the long run. It can actually strengthen it.

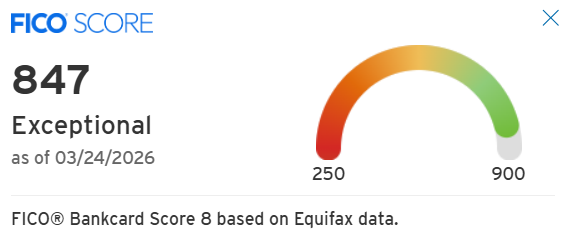

847 out of 850. Travel hacking didn't hurt my credit. It helped build it.

My credit score is higher now than it was before I started travel hacking over 20 years ago. That's not in spite of the strategy — it's partly because of it.

🛡️ What No One Tells You: The Honest Risks

Okay, here's where I'm going to be the friend who tells you the stuff the hype-y websites leave out. Because travel hacking does have real risks — they're just not the ones most people think of. And the good news? Every single one of them is manageable when you know what to watch for.

⚠️ It can lead to overspending if you're not careful

This is the biggest real risk, and I don't say that lightly.

If earning a welcome bonus tempts you to spend more than you normally would — buying things you don't need, inflating your lifestyle, putting charges on a card you can't pay off — then travel hacking becomes a net negative. Fast.

The golden rule: Never spend money you wouldn't already spend just to earn points. Points aren't "free" if they cost you interest payments or financial stress.

💬 Julie's honest take:

If you can't pay your full credit card balance every single month, travel hacking with new cards is not for you right now — and that's completely okay. It doesn't mean never. It means not yet. Get to a place where you're paying in full each month, and then come back to this strategy. It'll still be here.

💰 Annual fees can sneak up on you

Some travel cards come with annual fees ranging from $95 to $695. That first year is often offset by the welcome bonus and perks — but year two? That's when you need to do the math.

My take: only keep a card if the perks outweigh the fee. Do you actually use the lounge access? The travel credits? The free night certificate? If the answer is no, it's perfectly fine to downgrade to a no-annual-fee version or close the card. Know your numbers, and don't let fees pile up because you forgot to check.

Here's what I do: Every single year, when my annual fee hits, I sit down and re-evaluate that card. Is the free night certificate worth the fee? Am I using the lounge access? Do the travel credits cover it? If the perks outweigh the fee, I keep it. If they don't, I downgrade or cancel — no guilt, no loyalty to a piece of plastic.

📋 It takes organization

I won't sugarcoat this: travel hacking isn't hard, but it's not zero-effort, either.

You need to track due dates, know your minimum spending requirements and deadlines, and remember which card to use for which category. If you're someone who loses track of bills or avoids looking at your accounts, you'll want to build some systems first.

The good news? Tools make this incredibly simple. I recommend CardPointers— it tells you which card to use at every store, tracks your welcome bonus progress, and sends reminders. It takes the mental load from "overwhelming" to "basically on autopilot."

When I first started, I could keep track of everything in my head — which card earned what, when credits posted, which perks I'd used. But once I moved into premium cards with annual credits, quarterly bonuses, free night certificates, and rotating categories, my brain just couldn't keep up anymore. That's when I started using CardPointers, and honestly? It changed everything

⛔ It's not a good fit for everyone (right now)

I believe in being honest about this: there are situations where opening new credit cards is not the right move.

You carry credit card debt. Pay that down first. Interest charges will wipe out any points value.

You're applying for a mortgage within 6–12 months. New inquiries and accounts can raise questions during underwriting. Play it safe and wait.

You tend to impulse spend. If having a new card with a $5,000 limit feels like permission to spend $5,000, pause.

But here's the important thing: you can STILL earn points without opening new cards. Shopping portals, dining programs, optimizing the cards you already own — there's a whole world of travel hacking that doesn't touch your credit report. Which brings me to one of my favorite topics...

Travel Hacking Without Opening New Cards

This is a signature No Point Left Behind concept, and honestly? It's where I think most beginners should start.

If the idea of applying for new credit cards makes you nervous, you can still travel hack. You're probably already halfway there and don't even know it.

Here's what you can do right now — today — with what you already have:

Use shopping portals for everyday online purchases. Rakuten, airline shopping portals (like AAdvantage eShopping or the United MileagePlus portal) — you click through before you buy, and you earn bonus miles on purchases you were already making.

Join airline and hotel dining programs. Link your existing credit card to programs like Rapid Rewards Dining or Thank You Point Dining, and earn bonus points every time you eat out at participating restaurants.

Optimize the cards you already have. Most people don't use the right card for the right category. Your grocery card for groceries. Your dining card for restaurants. Your general card for everything else. Small change, big impact over time.

Stack deals. Portal bonus + credit card bonus category + sale price. This is where the magic happens — and it doesn't require a single new application.

Book through the right platforms to earn bonus points. Direct hotel bookings earn loyalty points; third-party sites often don't.

Join free loyalty programs. Hilton Honors, World of Hyatt, airline frequent flyer programs — they're all completely free to join. You start earning points on every stay and flight immediately.

💫 You're already halfway there.

If you shop online, eat at restaurants, stay at hotels, or fly even once or twice a year, you're leaving points on the table right now. The NPLB is just about capturing value you're already creating. No new cards needed. No credit impact. Just smarter spending.

✈️ 20 Years of Proof: Why I Trust This Strategy

I'm not sharing this stuff from a textbook. This is my life.

I've been travel hacking for over 20 years. I travel 12–15 times a year — with my sons, my best friend, my parents, my husband Brandon, and sometimes solo. And the vast majority of those trips are booked using points and miles.

Here are just a few highlights from our family's travel hacking journey:

🇮🇪 Free flights to Dublin for our 20th anniversary — booked entirely with points

🚢 Luxury cruise vacations using credit card points and strategic booking

🏨 Hotel stays at properties like Cloudland Resort in Georgia using Hilton points and Aspire free night certificates

🌎 Countless domestic and international trips — beaches, cities, mountain towns — all funded with points and miles

And through all of it? Our credit is excellent. Travel hacking didn't threaten our financial health; it's been a tool that works alongside it.

Every single trip featured on No Point Left Behind was booked this way. This isn't theory. This isn't hypothetical. This is what our family actually does — and has done for over two decades.

Travel hacking isn't just about saving money — it's about creating memories you couldn't afford otherwise.

✅ How to Start Safely: A Beginner Checklist

Ready to dip your toes in? Here's your safe, smart starting point — no overwhelm, no pressure to do it all at once:

Check your credit score. It's free at Credit Karma, through your bank app, or at annualcreditreport.com. Know where you stand before you do anything else.

Pay off any existing credit card balances first. Travel hacking and credit card debt don't mix. Get to zero, then start strategizing.

Set up autopay on every card — at least for the minimum payment, though paying in full is the goal. Never, ever miss a payment.

Start with ONE beginner-friendly card. Don't jump into five applications at once. Pick one card, learn the system, earn that first welcome bonus, and build confidence.

Only spend what you'd normally spend. Don't manufacture spending or buy things you don't need. Your regular bills, groceries, and gas are more than enough.

Track your due dates and minimum spend deadlines. Use a spreadsheet, a calendar reminder, or an app — whatever works for your brain.

Download CardPointers (or a similar tool) to optimize which card to use where. It takes the guesswork out of everyday purchases.

Join free loyalty programs for the airlines and hotels you actually use. Hilton Honors, World of Hyatt, Southwest Rapid Rewards — they're free and they start earning you points immediately.

Set a calendar reminder to evaluate annual fees before your card's renewal date. Give yourself time to decide: keep, downgrade, or cancel.

Read the No Point Left Behind Beginner Guide and Stack & Save Hub. I built these specifically to walk you through everything step by step — no jargon, no assumptions about what you already know.

🎯 The most important step?

Just start. You don't need to be perfect. You don't need to master everything at once. Even joining one loyalty program or shopping through one portal puts you ahead of 90% of travelers. Progress over perfection, always.

❓ FAQ: Your Biggest Travel Hacking Safety Questions

Is travel hacking legal?

Yes, 100%. Travel hacking is completely legal. You're using credit card rewards programs, loyalty points, and shopping portals exactly as they're designed to be used. Banks and airlines created these programs to attract customers — you're simply being a well-informed customer.

Will travel hacking hurt my credit score?

In the short term, opening a new card may cause a small, temporary dip of 5–10 points from the hard inquiry. But over time, responsible travel hacking typically improves your credit score by increasing your available credit (lowering utilization) and adding on-time payment history. The key word is "responsible" — always pay in full and on time.

Do I have to open new credit cards to travel hack?

Absolutely not. Opening new cards is one part of the strategy, but it's far from the only one. You can earn significant points through shopping portals, dining programs, free loyalty memberships, and optimizing the cards you already have. That's exactly what the "Lazy Girl Approach" is all about.

Is travel hacking worth it for small spenders?

Yes! You don't need to spend thousands of dollars a month. Shopping portals, dining programs, and free loyalty accounts earn you points on everyday spending. Even small, consistent efforts add up — especially when you stack deals. I've seen readers earn enough for a free hotel night just from holiday shopping through a portal.

Can travel hacking affect my mortgage application?

It can. If you're planning to apply for a mortgage within the next 6–12 months, I'd recommend holding off on opening new credit cards. Lenders look at recent inquiries and new accounts during underwriting. It's not that travel hacking is "bad" — it's just about timing. You can still use portals and loyalty programs during this time.

What happens if I can't meet the minimum spend?

If you don't meet the minimum spend requirement within the specified timeframe, you simply won't earn the welcome bonus — but you won't be penalized or charged extra. That's why I always say: only apply for a card when your natural spending will cover the requirement. Don't stretch for it.

Are points and miles really "free"?

Points themselves don't cost you money if you're earning them on spending you'd do anyway. However, they're not entirely "free" — there may be annual fees, and you're investing your time in learning the system. The value equation is overwhelmingly positive for most people, but it's honest to acknowledge the small costs involved.

How do I know if travel hacking is right for me?

Ask yourself: Do I pay my credit card bills in full each month? Am I comfortable tracking a few due dates? Do I travel (or want to travel) at least once or twice a year? If you answered yes to all three, travel hacking is almost certainly a good fit. If you're not there yet, start with the no-new-cards approach and build from there.

💬 You Don't Have to Figure This Out Alone

Learning travel hacking is so much easier when you've got a community behind you. I started the Travel Hacking Moms Group on Facebook as a space for moms (and honestly, anyone) who want to learn the ropes without judgment, ask questions without feeling silly, and celebrate those first free flights together.

We share tips, cheer each other on, and nobody gatekeeps. Whether you're brand new or you've been stacking points for years, you're welcome here.

👉 Join the Travel Hacking Moms Group on Facebook

It's free, it's supportive, and it might just be the thing that gives you the confidence to book your first points trip.

💚 The Bottom Line

So — is travel hacking safe?

Yes. When done responsibly, travel hacking is safe, legal, and genuinely one of the smartest things you can do with your everyday spending.

It's not a scam. It's not a scheme. And it's not too good to be true. It's just being intentional about how you spend, where you click, and which card you pull out of your wallet.

The banks are going to make money either way. The airlines are going to sell those seats. The hotels are going to fill those rooms. You might as well make sure YOU benefit, too.

I've been doing this for over 20 years. My family has visited places we never could have afforded at retail prices. My kids have seen the world. Brandon and I have celebrated anniversaries in countries we used to just dream about. And we did it all without going into debt, without ruining our credit, and without doing anything remotely shady.

If you're a beginner and you're nervous — that's normal. Start small. Read the Beginner Guide. Ask questions. You don't have to do everything at once.

But please — don't let fear keep you from a strategy that could genuinely change the way your family travels.

The best time to start travel hacking was years ago. The second best time is right now. And I'm here to walk you through every step. — Julie

👉 Ready to take the first step? Head over to the No Point Left Behind Beginner Guide for a complete, step-by-step walkthrough — written for people who are starting from absolute zero. No jargon. No assumptions. Just a clear path to your first free trip.

Disclosure: This post contains an affiliate link to CardPointers. If you sign up through my link, I may earn a small commission at no extra cost to you. This post does not contain credit card affiliate links — I never use them. Any credit card links on this site are my personal referral links, which I clearly identify. I'm not a financial advisor, financial planner, or CPA — I'm a travel-hacking mom sharing strategies that have worked for my family. This content is for educational and informational purposes only and should not be considered personal financial advice. Please consult a qualified financial professional for decisions about your individual situation.

Julie Davis is the creator of No Point Left Behind, where she helps travelers turn everyday spending into unforgettable trips through simple, beginner-friendly points and miles strategies. She's a mom, a deal-stacking pro, and a firm believer that luxury travel doesn't have to come with a luxury price tag.