🌟 How to Choose Your First Card (Without Feeling Overwhelmed)

Your simple, beginner‑friendly guide to picking the right card for your goals — not someone else’s.

By Julie Davis · Updated May 2026

Disclosure: This post contains affiliate and personal referral links. I’m not a credit card affiliate — any credit card links you see here are my own personal referral links, which may earn me bonus points if you choose to use them. Other links may earn me a small commission at no extra cost to you. I only share cards, tools, and strategies we personally use and trust.

💳 Why Choosing Your First Card Matters

Your first card sets the tone for your entire points journey. Pick one that fits your lifestyle — not the internet’s idea of “best.”

The right card should feel easy to manage, earn flexible rewards, and help you build confidence without pressure.

🧭 Step 1: Know Your Goal

Before you even look at cards, ask yourself one question:

“What do I want my points to do for me?”

Travel more often? → Focus on flexible points (Chase Ultimate Rewards, Amex Membership Rewards).

Save money on everyday purchases? → Look for cash‑back cards.

Stay at specific hotels or fly one airline? → Consider co‑branded cards once you’ve learned the basics.

👉 Read next: Beginner Credit Card Guide (2026) — your full roadmap for starting safely.

🟦 Step 2: Start Simple

You don’t need ten cards or a spreadsheet. Start with one beginner‑friendly card that earns flexible points and has perks you’ll actually use.

My favorites for beginners:

Chase Sapphire Preferred — simple, safe, and flexible for travel.

Capital One Venture — easy redemptions and strong everyday earning.

Chase Freedom Unlimited — great for families and students starting out.

👉 See my full list: Best Beginner Credit Cards for 2026

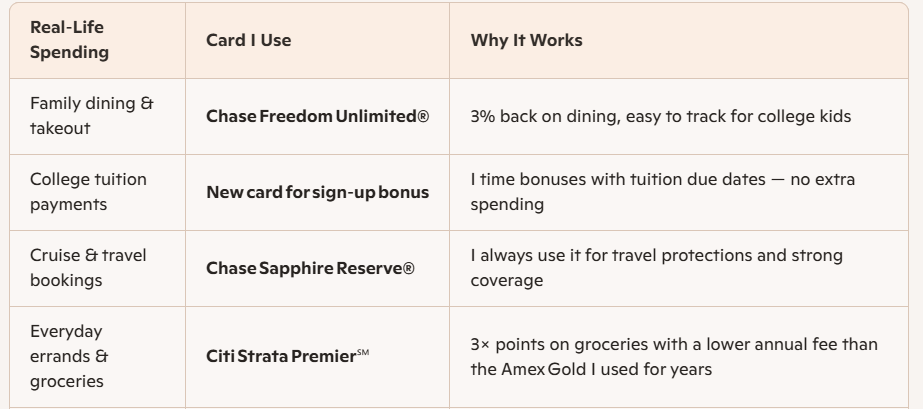

🟩 Step 3: Match the Card to Your Spending

Think about where your money already goes — that’s where your points should come from. These are the cards I personally use for these categories

👉 Related post:How to Stack Dining Credits for Double or Triple Points

🟨 Step 4: Understand Perks vs Risks

Every perk has a purpose — but not every perk is worth chasing.

✅ Worth it:

Travel insurance

Transferable points

Dining credits you’ll actually use

🚫 Skip it:

Complicated airline status programs

Credits you forget to redeem

Cards with high fees and low return

👉 Read next: Unpacking Credit Card Perks vs Risks (2026)

🟧 Step 5: Keep It Manageable

Start slow. Track your perks and credits with CardPointers — it keeps everything organized so you never miss a benefit.

👉 See how I use it: CardPointers Review + How I Use It

🟪 Step 6: Build Confidence, Not Stress

Your first card should make you feel empowered, not overwhelmed. Once you’ve learned how it works, you can layer in a second card that complements your spending — not duplicates it.

👉 Next step: Stack & Save Credit Card Hub

🧳 Real‑Life Example

When I first started, I chose the Chase Sapphire Preferred because it was simple, flexible, and beginner‑friendly. It helped me earn my first free flight — and eventually, it became the foundation for our family’s travel strategy.

💡 Pro Tip

Don’t chase perfection — chase progress. The best card is the one that fits your life right now.

👋 About Julie

I’m Julie — creator of No Point Left Behind, mom of two college boys, and a travel‑hacking strategist who believes travel should feel simple, affordable, and fun. I teach beginners how to use points, perks, and smart planning to travel more without spending more.